- Italian government issues dissipate; Euro vulnerable with ECB later today.

- Commodity bloc breaks down – a sign of risk-aversion looming.

INTRADAY PERFORMANCE UPDATE: 09:30 GMT

MAJORS

| |||||||

(vs USD)

|

-0.50%

|

-0.19%

|

+0.10%

|

+0.05%

|

+0.10%

|

+0.52%

|

-0.47%

|

ASIA/EUROPE FOREX NEWS WRAP

Frustrated by Prime Minister Shinzo Abe’s fiscal stimulus plans, investors have ditched risk assets and turned back to the Japanese Yen as the favored safe haven amid gathering storm clouds in Europe and North America. While the Italian political debacle evolves – it appears that Prime Minister Enrico Letta will retain the coalition, but will lose overall support in the Senate – the US fiscal debate looms large, aiding the shift into ‘safer’ assets.

The United States’ own political turmoil is just starting to permeate markets, with Markit Economics, the firm behind the global PMI surveys, noting that the CDS curve for US government debt has inverted (1Y CDS > 5Y CDS) for the first time since July 2011 – an ominous sign indeed. With fears that the funding showdown could spill over into a cantankerous debt ceiling fight, the Yen has been duly aided by slipping US equity markets and strengthening US Treasuries.

The Yen’s next big move could come against the Euro today as the European Central Bank meets. While the policy decision itself is expected to be bland – no change in any rates, no changes to any non-standard measures – all eyes are on ECB President Mario Draghi’s press conference at 08:30 EDT/12:30 GMT.

Whereas Euro-Zone data ticked higher midyear, recent economic reports suggest that the rebound may be cooling off. Most notably, Euro-Zone inflation has fallen back to its lowest level since February 2011, a post-GFC low; and Euro-Zone banks’ capital levels (via excess reserves) have receded back to December 2011 levels. This adds up to weak credit growth, which ECB President Draghi has and will continue to harp on (which was EUR-negative in August).

Accordingly, we don’t expect another LTRO – the measure used to help banks restart lending vis-à-vis capital injections – but the ECB should outline all of the data that suggest another one might be useful over the coming months. As such, we believe the Euro will be highly-sensitive to any dovish rhetoric with risks skewed to the downside amid any indication that the ECB is considering a third LTRO.

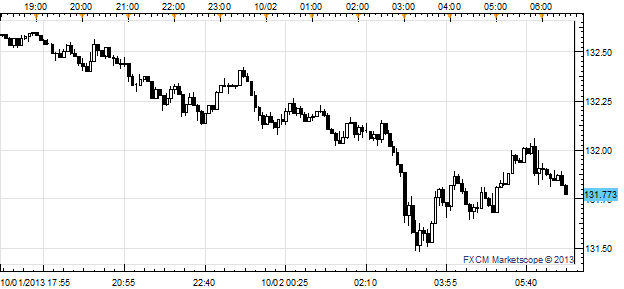

EURJPY 5-minute Chart: October 2, 2013 Intraday

Taking a look at European credit, reports that Italian PM Letta will retain control have helped lift the Euro as near-term political risks have seemingly abated. The Italian 2-year note yield has decreased to 1.679% (-6.3-bps) while the Spanish 2-year note yield has increased to 1.355% (+2.3-bps). Likewise, the Italian 10-year note yield has decreased to 4.345% (-6.4-bps) while the Spanish 10-year note yield has increased to 4.195% (+4.0-bps); lower yields imply higher prices

ECONOMIC CALENDAR – UPCOMING NORTH AMERICAN SESSION

Source:

No comments:

Post a Comment